Schedule 36 notices issued offshore: validity, enforcement and practical risk

Written by

Dan Smitten

5 min read

Updated - June 29, 2026

HMRC can issue information notices to UK taxpayers outside the UK, but the practical risks often lie less in the validity of the notice and more in how the enquiry develops.

Why this matters now

We have seen an uptick in informal information requests to offshore entities in connection with UK taxpayers. Whilst these are informal requests, it is worth considering the formal powers underlying these HMRC requests.

Notices issued under Schedule 36 Finance Act 2008 (Schedule 36) are the most commonly used of HMRC’s information gathering powers.

The judgment in the case of R (Jimenez) v First-Tier Tribunal and HMRC, confirmed that HMRC can issue notices under Schedule 36, to an address outside the UK.

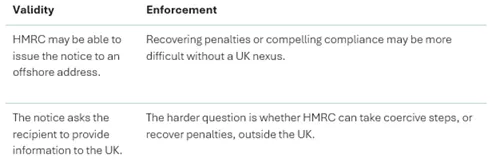

Whilst HMRC can validly issue a Schedule 36 taxpayer notice to a person abroad, their ability to practically enforce the notice is much more complicated. Even though enforcement is difficult, there are still significant risks arising from the receipt of a notice by an entity abroad.

At a glance

-

HMRC can validly issue a Schedule 36 taxpayer notice to a UK taxpayer outside the UK.

-

Enforcement abroad may be more difficult, particularly where there is no UK nexus.

-

Non-compliance can still affect penalties, assessments and HMRC’s future approach.

The practical question is not only whether the notice is valid, but how the recipient responds.

What is a Schedule 36 notice?

HMRC in most cases will write out to a taxpayer for information on an informal basis in the first instance. In rare scenarios, for example where HMRC suspect fraud or where there is previous non-compliance, they could move straight to their formal powers.

If HMRC do not receive a response to an informal request or receive a partial response they could then seek to use their formal statutory powers to request information and documents that are reasonably required for the purpose of checking a taxpayer’s tax position.

There are various routes to challenge a Schedule 36 notice, and restrictions on what HMRC can include in the request, which we cover further in our guide on Schedule 36 notices.

The two common forms of Schedule 36 notice considered here are:

- A taxpayer notice / 1st party notice – a request for information from the taxpayer into which HMRC are enquiring.

- A third-party notice / 3rd party notice – a request information from a 3rd party to allow them to check the tax position of another taxpayer.

What Jimenez decided

Case at a glance

- The notice was issued to Mr Jimenez at his address in Dubai.

- The information requested included bank details and UK visit history as part of a check into his tax

residence position. - The Court of Appeal held that HMRC were entitled to issue information notices to UK taxpayers living outside the UK.

R (Jimenez) vs The First-Tier Tribunal and HMRC, was a decision handed down by the Court of Appeal in 2019, following the initial successful challenge by the taxpayer through judicial review.

The case involved a Schedule 36 notice issued to Mr Jimenez at his address in Dubai, for information including bank details and UK visit history as part of a check into his tax residence position.

The First-Tier Tribunal had approved the notice, following a without notice application by HMRC, finding that the information was reasonably required for HMRC’s enquiry.

However, the High Court under judicial review quashed the notice and held that HMRC’s Schedule 36 powers were limited to the UK.

HMRC appealed this decision to the Court of Appeal, which held that HMRC were entitled to issue information notices to UK taxpayers living outside the UK. The explanation concluded that the powers under Schedule 36 depend on the recipient’s status as a UK taxpayer, not their location.

The powers under Schedule 36 depend on the recipient’s status as a UK taxpayer, not their location.

This decision will be seen as binding by HMRC and confirms that a 1st party notice issued by HMRC to a taxpayer offshore is a valid information notice.

In the judgment, the Court of Appeal said that it was clear that parliament had not intended for the scope of each individual provision of Schedule 36 to be the same.

Validity and enforcement are different questions

Whilst it is therefore clear that HMRC can issue a 1st party notice under Schedule 36 to an offshore address, what is far less clear is their ability to actually enforce the notice, although this position is assisted by any UK nexus.

The court made clear the difference between issuing a notice, and enforcement, and the notice in the case of R (Jimenez) was valid because it does not require any coercive act in a foreign country but rather just asks the individual to provide information to the UK.

HMRC’s usual route to compliance with a Schedule 36 notice would be to issue penalties, however these penalties are primarily enforceable on UK assets or persons. Where an individual is not based in the UK, and holds no UK assets, HMRC may struggle to recover any penalties.

There are, however, other impacts of the notice that should be considered.

Why offshore recipients should not ignore the notice

The practical consequences may include:

- Non-compliance with a HMRC notice will have an impact if assessments are raised.

- This has a direct impact on the reduction HMRC provides for penalties and will result in more significant penalties.

- In assessments featuring careless behaviour, this could also prevent the option for HMRC to suspend penalties.

- HMRC will also factor in behaviour when looking forward to further enquiries, they may, for example, move more quickly to formal powers in cases where they have previously encountered non-compliance.

Exchange of information and third-party routes

Where HMRC have issued a Schedule 36 notice to a non-UK based individual, it is also worth considering the other steps they are taking, and HMRC lays out some of these options in their guidance at [CH223150

- How to do a compliance check: information powers: taxpayer notice: address

outside UK](https://www.gov.uk/hmrc-internal-manuals/compliance-handbook/ch223150).

For an Exchange of Information request, HMRC have to show that they have exhausted all domestic avenues to obtain the information before reaching out to another country, however the guidance is clear that the officer leading the enquiry should be in contact with the Exchange of Information team at an early stage, which would likely be before they are issuing notices under Schedule 36.

HMRC would also already be considering reaching out to 3rd parties that they think may hold relevant information within the UK, whether that is through financial institutions or other sources, such as customers or suppliers. There is a natural fear regarding reputational damage in these scenarios.

The practical risk: losing control of the enquiry

There is also the more aggressive route from HMRC. If HMRC believe that they have sufficient information to justify making a best judgment assessment, they can move straight to raising an assessment for the tax due. This would naturally encourage an appeal from the taxpayer who will then need to provide evidence in support of their appeal, which would contain the information HMRC have requested.

Whilst the enforcement issue may still exist for HMRC, where there is any potential UK nexus this could bring significant financial risks.

Conclusion

In practice, the position after Jimenez is not about whether HMRC can issue an information notice offshore, but more about what the recipient chooses to do on receipt. Even though HMRC may struggle to enforce such notices, taxpayers cannot and should not just ignore them.

Penalties can accrue and be brought to bear where there is a UK connection, either presently or in the future. More importantly, non-compliance could shift enquiries into HMRC’s favour, providing a strong basis for movement to more formal powers and increased assessments.

HMRC are entitled to request information to confirm a taxpayer’s position is correct, however they are not entitled to ask for whatever information they want to and must have a legal basis for the request.

The real risk with a Schedule 36 notice issued to an offshore taxpayer does not lie with the validity of the notice itself, but rather how to ensure that the enquiry does not widen and grow outside of the taxpayer’s control.